AI Projects Stall. Ours Go Live.

AI Accelerators are our starting point — pre-built AI systems we tailor to your data and deploy directly into enterprise workflows.

We help you validate value before full-scale build, so decisions are grounded in real operational data, not assumptions.

Precision-built. Enterprise-ready. Designed for regulated life sciences environments.

Adds months to project.

Built with confidence.

Pre-Built AI Systems.

Deployed for Life Sciences.

The Precision Instrument for MDP Compliance

Fine-tuned on the Manufacturer Discount Program. Liability modeling, phase-in analysis, and regulatory Q&A with verbatim citations — purpose-built for the IRA era.

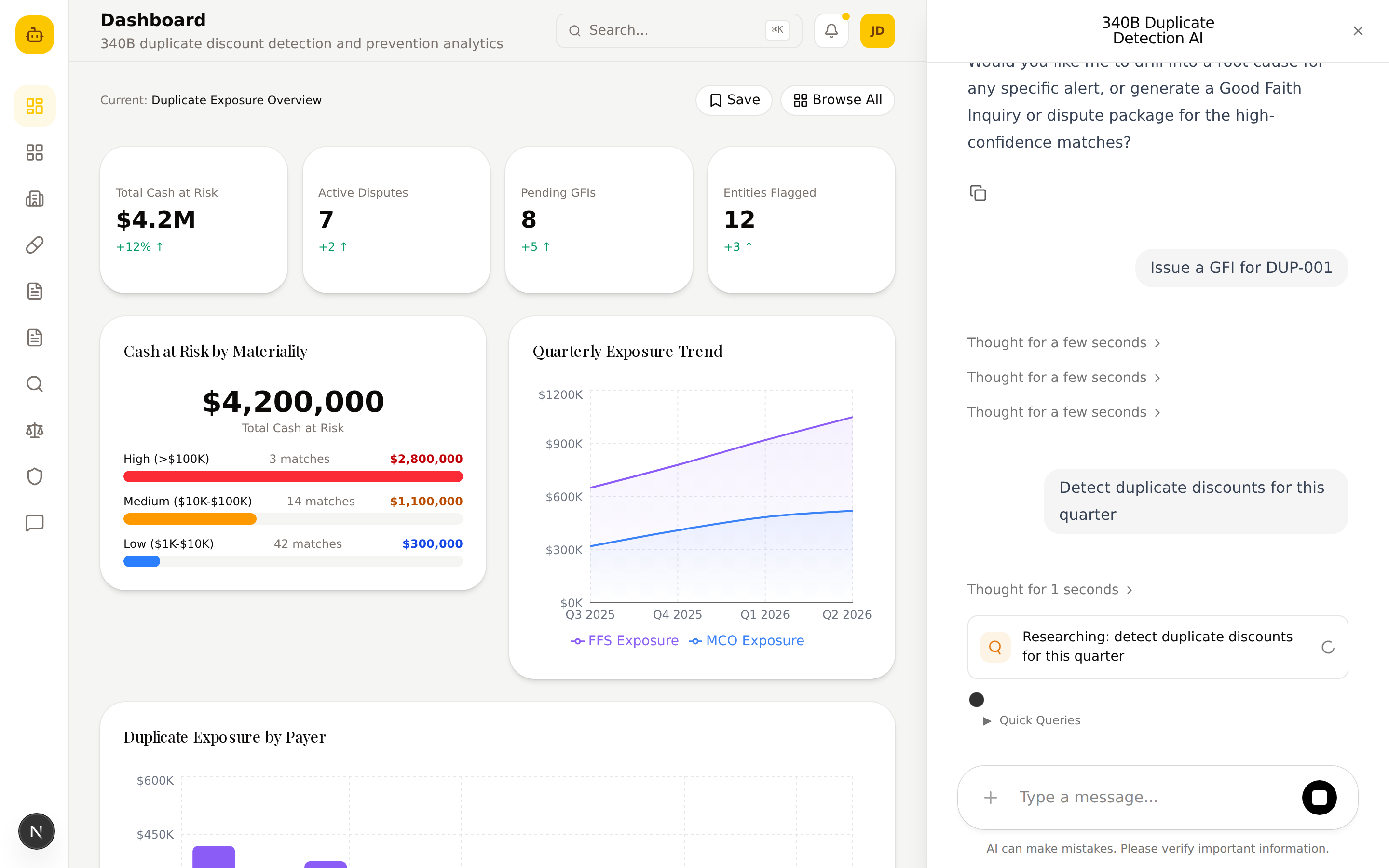

Duplicate discount prevention with conversational data access

Ask in plain English. Get alert cards with confidence scores, root cause diagnoses, and one-click resolution. No batch windows. No training.

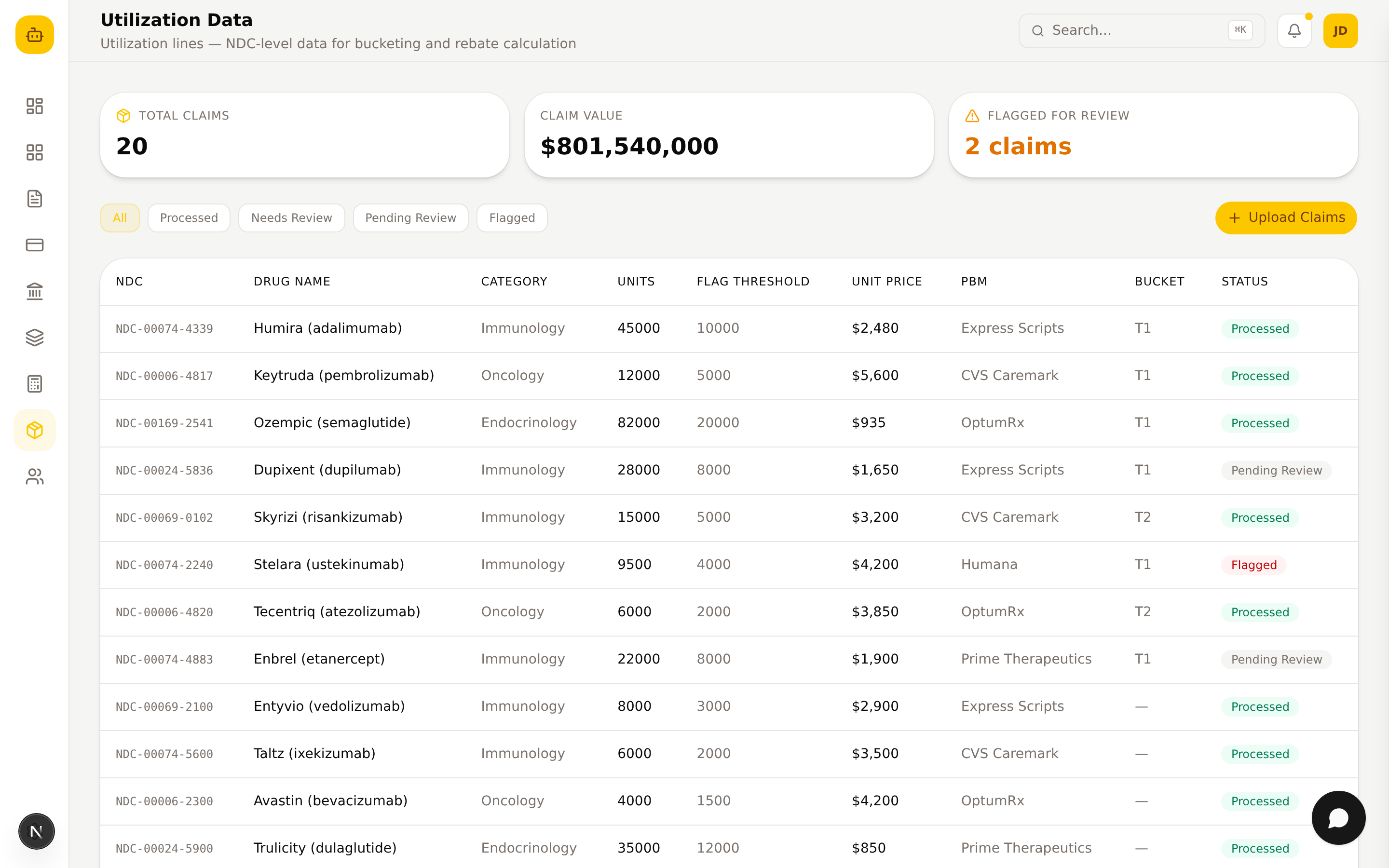

The full rebate lifecycle — conversational, real-time, one system

Accruals, payments, claims bucketing, and reconciliation in one real-time dashboard. Ask questions in plain English. Get instant answers with charts. No SQL. No report writers.

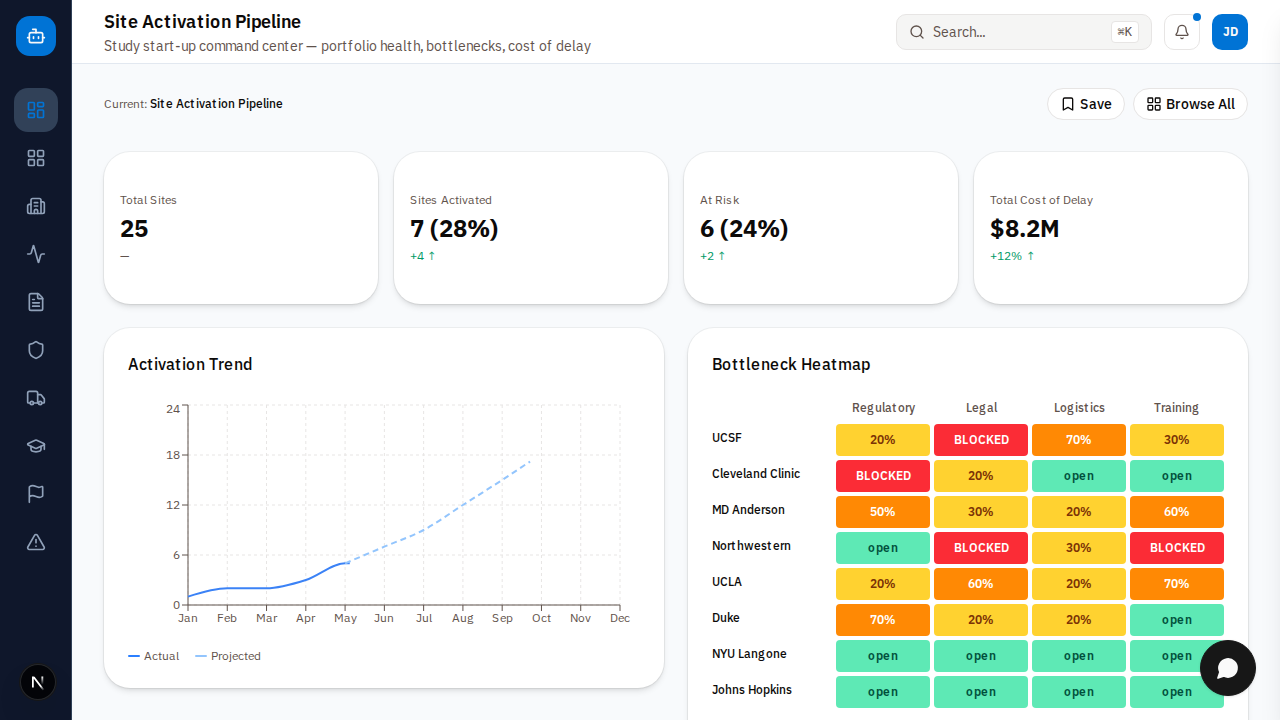

AI-native clinical trial site activation — in one conversation

Diagnose stalled sites, model cascade impact across Regulatory, Legal, Logistics, and Training workstreams, and orchestrate resolutions — all through conversation. Pipeline KPIs with cost of delay. One-click HITL approvals.

This answers a critical need in a way that no other solution in the marketplace does.

Affirmed the regulatory and technical architecture of both the KugelOne and HelixIQ² platforms.

Latest Analysis

Regulatory analysis and industry perspectives shaping life sciences decision-making.

Browse InsightsSchedule an AI Discovery Call

Tell us about the problem you're solving. We'll show you which AI Accelerator fits and how we deploy it. No pressure. Just expertise.